All Categories

Featured

Table of Contents

The strategy has its very own advantages, but it also has problems with high fees, intricacy, and extra, resulting in it being considered a fraud by some. Unlimited financial is not the best policy if you require only the financial investment part. The limitless financial idea revolves around the use of entire life insurance policy policies as a monetary device.

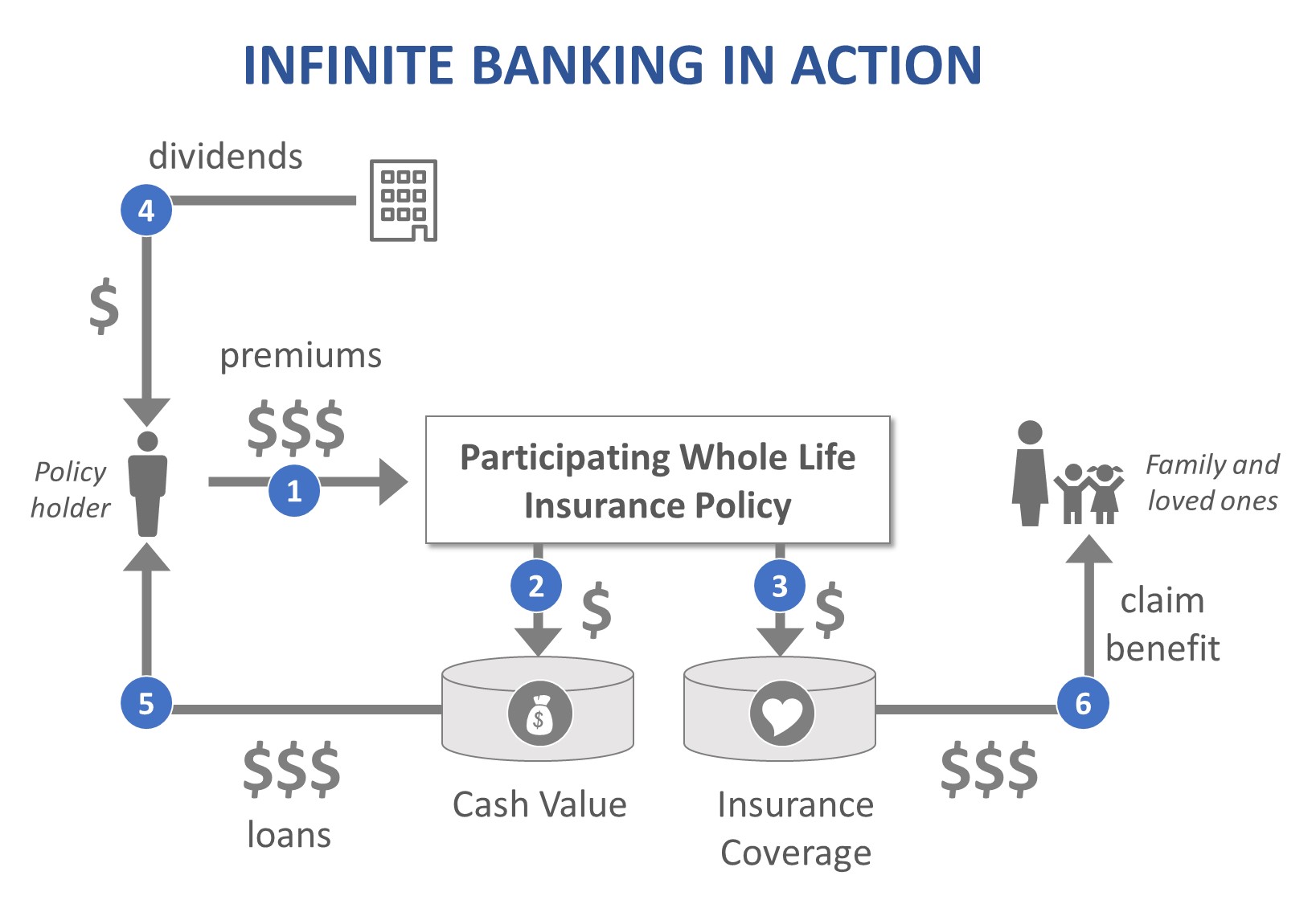

A PUAR permits you to "overfund" your insurance plan right up to line of it becoming a Customized Endowment Agreement (MEC). When you use a PUAR, you swiftly boost your cash value (and your survivor benefit), therefore raising the power of your "financial institution". Further, the more cash worth you have, the better your rate of interest and reward repayments from your insurance provider will certainly be.

With the rise of TikTok as an information-sharing platform, economic advice and techniques have actually discovered an unique method of spreading. One such technique that has been making the rounds is the boundless banking principle, or IBC for short, amassing endorsements from stars like rap artist Waka Flocka Flame - Wealth management with Infinite Banking. However, while the approach is currently popular, its roots trace back to the 1980s when economist Nelson Nash introduced it to the globe.

What is the minimum commitment for Infinite Wealth Strategy?

Within these policies, the cash money value expands based on a rate set by the insurance firm. Once a considerable cash value gathers, policyholders can acquire a cash value financing. These finances differ from conventional ones, with life insurance policy working as collateral, implying one could lose their coverage if loaning excessively without adequate cash money worth to sustain the insurance coverage prices.

And while the appeal of these plans appears, there are innate constraints and dangers, necessitating persistent cash money value surveillance. The technique's legitimacy isn't black and white. For high-net-worth people or organization owners, specifically those utilizing techniques like company-owned life insurance coverage (COLI), the advantages of tax obligation breaks and compound growth could be appealing.

The attraction of unlimited financial doesn't negate its challenges: Price: The foundational demand, an irreversible life insurance coverage plan, is costlier than its term counterparts. Eligibility: Not everyone receives entire life insurance policy as a result of extensive underwriting processes that can omit those with specific health and wellness or way of life problems. Intricacy and danger: The intricate nature of IBC, coupled with its threats, may hinder lots of, specifically when easier and much less dangerous options are available.

Who can help me set up Financial Independence Through Infinite Banking?

Assigning around 10% of your regular monthly earnings to the policy is just not viable for the majority of people. Making use of life insurance policy as an investment and liquidity resource needs self-control and tracking of policy cash money worth. Speak with a financial consultant to determine if boundless banking straightens with your priorities. Part of what you read below is simply a reiteration of what has currently been said above.

So prior to you obtain into a scenario you're not planned for, know the following first: Although the principle is commonly sold as such, you're not in fact taking a lending from yourself. If that held true, you would not need to repay it. Rather, you're borrowing from the insurance provider and have to settle it with passion.

Some social media posts advise using money value from whole life insurance policy to pay down credit score card debt. When you pay back the funding, a section of that rate of interest goes to the insurance firm.

What is Infinite Banking For Financial Freedom?

For the first a number of years, you'll be repaying the commission. This makes it incredibly tough for your policy to collect value throughout this moment. Entire life insurance policy costs 5 to 15 times much more than term insurance policy. Lots of people just can't manage it. So, unless you can manage to pay a few to several hundred bucks for the following decade or even more, IBC won't work for you.

Not everybody must rely exclusively on themselves for monetary safety. Infinite Banking for financial freedom. If you require life insurance policy, right here are some important tips to think about: Consider term life insurance policy. These plans provide protection during years with significant monetary responsibilities, like home loans, trainee fundings, or when taking care of children. Make certain to search for the ideal price.

What are the most successful uses of Financial Independence Through Infinite Banking?

Visualize never ever having to worry about small business loan or high passion prices once more. What if you could obtain cash on your terms and build wide range all at once? That's the power of infinite banking life insurance policy. By leveraging the money value of whole life insurance policy IUL policies, you can grow your wealth and borrow money without counting on traditional banks.

There's no set loan term, and you have the freedom to determine on the repayment schedule, which can be as leisurely as paying back the finance at the time of death. This adaptability prolongs to the servicing of the car loans, where you can choose for interest-only settlements, keeping the finance balance level and workable.

How secure is my money with Infinite Banking Retirement Strategy?

Holding money in an IUL dealt with account being credited passion can commonly be much better than holding the cash on down payment at a bank.: You have actually constantly fantasized of opening your very own bakeshop. You can borrow from your IUL plan to cover the first costs of renting out a space, acquiring tools, and working with staff.

Individual financings can be gotten from traditional banks and credit score unions. Obtaining money on a credit score card is usually really expensive with annual percentage rates of rate of interest (APR) typically getting to 20% to 30% or more a year.

{kind=link}

Latest Posts

Whole Life Concept

Non Direct Recognition Insurance Companies

5 Steps To Be Your Own Bank With Whole Life Insurance