All Categories

Featured

Table of Contents

The approach has its own advantages, but it likewise has problems with high costs, complexity, and more, leading to it being pertained to as a scam by some. Boundless financial is not the finest policy if you need only the investment component. The limitless banking idea rotates around the use of whole life insurance policy policies as an economic tool.

A PUAR enables you to "overfund" your insurance coverage right approximately line of it becoming a Changed Endowment Agreement (MEC). When you make use of a PUAR, you rapidly enhance your money worth (and your survivor benefit), thus increasing the power of your "bank". Further, the even more cash worth you have, the higher your rate of interest and dividend settlements from your insurance coverage business will be.

With the surge of TikTok as an information-sharing platform, monetary suggestions and techniques have actually discovered a novel means of spreading. One such approach that has been making the rounds is the unlimited banking concept, or IBC for brief, gathering endorsements from celebs like rapper Waka Flocka Flame - Infinite Banking for financial freedom. Nevertheless, while the technique is currently prominent, its origins trace back to the 1980s when financial expert Nelson Nash introduced it to the world.

What makes Self-financing With Life Insurance different from other wealth strategies?

Within these policies, the cash value grows based on a rate established by the insurance provider. When a significant cash money value collects, insurance policy holders can acquire a cash money value funding. These fundings differ from traditional ones, with life insurance policy functioning as collateral, indicating one could shed their insurance coverage if borrowing exceedingly without adequate money worth to sustain the insurance policy prices.

And while the allure of these policies is evident, there are inherent restrictions and threats, demanding thorough cash money worth surveillance. The technique's authenticity isn't black and white. For high-net-worth individuals or local business owner, especially those using strategies like company-owned life insurance coverage (COLI), the advantages of tax obligation breaks and substance growth might be appealing.

The attraction of unlimited banking doesn't negate its difficulties: Price: The foundational demand, a permanent life insurance coverage plan, is more expensive than its term counterparts. Eligibility: Not everyone receives whole life insurance policy due to extensive underwriting processes that can leave out those with certain wellness or lifestyle conditions. Intricacy and threat: The intricate nature of IBC, combined with its threats, might deter several, particularly when simpler and less high-risk options are readily available.

What are the common mistakes people make with Tax-free Income With Infinite Banking?

Alloting around 10% of your monthly revenue to the policy is just not viable for the majority of people. Utilizing life insurance policy as a financial investment and liquidity resource requires technique and tracking of plan cash value. Speak with a monetary advisor to establish if limitless financial straightens with your top priorities. Component of what you review below is merely a reiteration of what has actually currently been claimed above.

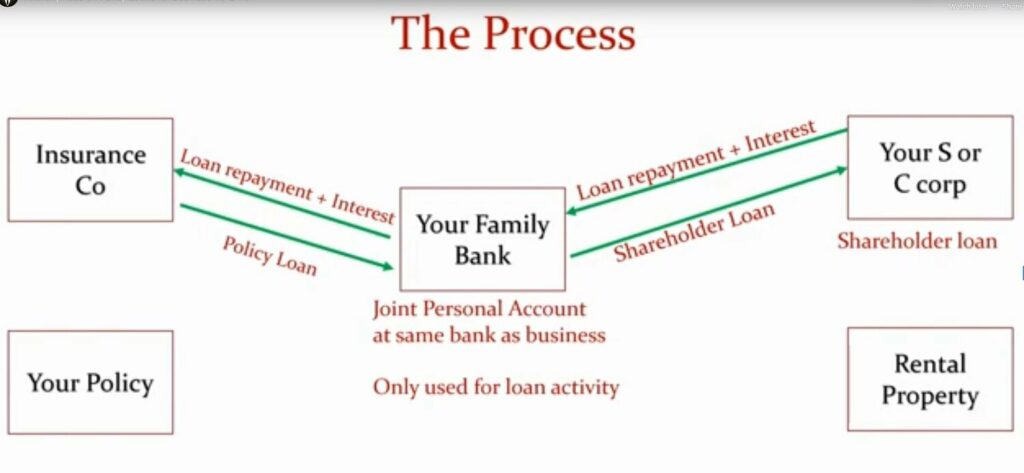

So prior to you obtain right into a circumstance you're not gotten ready for, understand the complying with first: Although the idea is typically marketed therefore, you're not actually taking a lending from on your own. If that held true, you wouldn't have to repay it. Rather, you're obtaining from the insurance policy firm and have to settle it with passion.

Some social media blog posts advise utilizing cash money value from entire life insurance policy to pay for credit score card financial obligation. The concept is that when you pay off the loan with rate of interest, the quantity will certainly be sent out back to your investments. That's not just how it works. When you pay back the financing, a section of that passion mosts likely to the insurance provider.

How can Policy Loan Strategy reduce my reliance on banks?

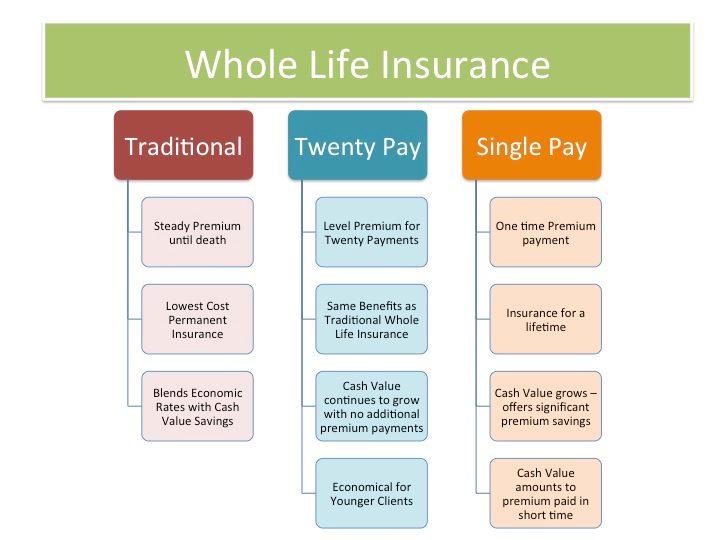

For the initial several years, you'll be paying off the commission. This makes it extremely hard for your plan to accumulate worth during this time around. Whole life insurance coverage prices 5 to 15 times extra than term insurance. The majority of people merely can not afford it. Unless you can manage to pay a couple of to numerous hundred dollars for the next years or even more, IBC will not function for you.

If you call for life insurance policy, right here are some important pointers to take into consideration: Think about term life insurance policy. Make sure to go shopping about for the finest price.

How do interest rates affect Generational Wealth With Infinite Banking?

Think of never having to worry regarding bank loans or high interest rates once again. That's the power of unlimited banking life insurance.

There's no set loan term, and you have the freedom to choose the repayment routine, which can be as leisurely as repaying the lending at the time of death. This adaptability encompasses the servicing of the finances, where you can go with interest-only payments, maintaining the car loan equilibrium level and workable.

How do I qualify for Leverage Life Insurance?

Holding money in an IUL repaired account being credited interest can frequently be far better than holding the cash on down payment at a bank.: You have actually constantly dreamed of opening your own bakeshop. You can obtain from your IUL policy to cover the initial expenses of renting a space, acquiring devices, and working with staff.

Individual car loans can be acquired from typical banks and lending institution. Right here are some bottom lines to take into consideration. Credit report cards can supply a flexible means to borrow money for really temporary durations. Nonetheless, obtaining cash on a bank card is typically extremely costly with interest rate of interest (APR) commonly getting to 20% to 30% or more a year.

{kind=link}

Latest Posts

Whole Life Concept

Non Direct Recognition Insurance Companies

5 Steps To Be Your Own Bank With Whole Life Insurance